Page 142 - InterloopAnnualReport2020

P. 142

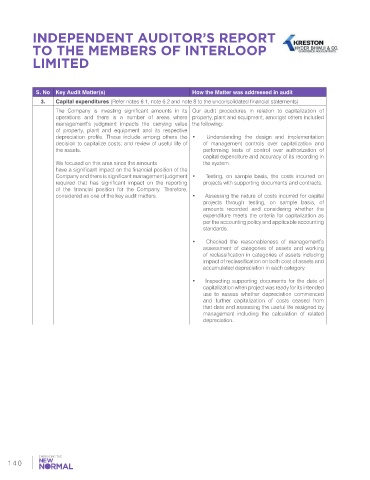

INDEPENDENT AUDITOR’S REPORT

TO THE MEMBERS OF INTERLOOP

LIMITED

S. No Key Audit Matter(s) How the Matter was addressed in audit

3. Capital expenditures (Refer notes 6.1, note 6.2 and note 8 to the unconsolidated financial statements)

The Company is investing significant amounts in its Our audit procedures in relation to capitalization of

operations and there is a number of areas where property, plant and equipment, amongst others included

management’s judgment impacts the carrying value the following:

of property, plant and equipment and its respective

depreciation profile. These include among others the • Understanding the design and implementation

decision to capitalize costs; and review of useful life of of management controls over capitalization and

the assets. performing tests of control over authorization of

capital expenditure and accuracy of its recording in

We focused on this area since the amounts the system.

have a significant impact on the financial position of the

Company and there is significant management judgment • Testing, on sample basis, the costs incurred on

required that has significant impact on the reporting projects with supporting documents and contracts.

of the financial position for the Company. Therefore,

considered as one of the key audit matters. • Assessing the nature of costs incurred for capital

projects through testing, on sample basis, of

amounts recorded and considering whether the

expenditure meets the criteria for capitalization as

per the accounting policy and applicable accounting

standards.

• Checked the reasonableness of management’s

assessment of categories of assets and working

of reclassification in categories of assets including

impact of reclassification on both cost of assets and

accumulated depreciation in each category.

• Inspecting supporting documents for the date of

capitalization when project was ready for its intended

use to assess whether depreciation commenced

and further capitalization of costs ceased from

that date and assessing the useful life assigned by

management including the calculation of related

depreciation.

140