Page 189 - InterloopAnnualReport2020

P. 189

NOTES TO THE UNCONSOLIDATED

FINANCIAL STATEMENTS

For the year ended June 30, 2020

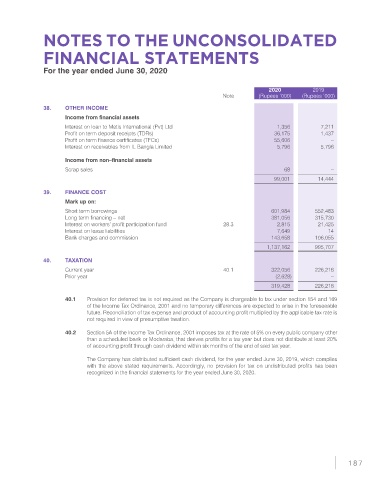

2020 2019

Note (Rupees ‘000) (Rupees ‘000)

38. OTHER INCOME

Income from financial assets

Interest on loan to Metis International (Pvt) Ltd 1,356 7,211

Profit on term deposit receipts (TDRs) 36,175 1,437

Profit on term finance certificates (TFCs) 55,606 –

Interest on receivables from IL Bangla Limited 5,796 5,796

Income from non–financial assets

Scrap sales 68 –

99,001 14,444

39. FINANCE COST

Mark up on:

Short term borrowings 601,984 552,483

Long term financing – net 381,056 315,730

Interest on workers’ profit participation fund 28.3 2,815 21,425

Interest on lease liabilities 7,649 14

Bank charges and commission 143,658 106,055

1,137,162 995,707

40. TAXATION

Current year 40.1 322,056 226,216

Prior year (2,628) –

319,428 226,216

40.1 Provision for deferred tax is not required as the Company is chargeable to tax under section 154 and 169

of the Income Tax Ordinance, 2001 and no temporary differences are expected to arise in the foreseeable

future. Reconciliation of tax expense and product of accounting profit multiplied by the applicable tax rate is

not required in view of presumptive taxation.

40.2 Section 5A of the Income Tax Ordinance, 2001 imposes tax at the rate of 5% on every public company other

than a scheduled bank or Modaraba, that derives profits for a tax year but does not distribute at least 20%

of accounting profit through cash dividend within six months of the end of said tax year.

The Company has distributed sufficient cash dividend, for the year ended June 30, 2019, which complies

with the above stated requirements. Accordingly, no provision for tax on undistributed profits has been

recognized in the financial statements for the year ended June 30, 2020.

187