Page 253 - InterloopAnnualReport2020

P. 253

NOTES TO THE CONSOLIDATED

FINANCIAL STATEMENTS

For the year ended June 30, 2020

26.7 The Holding Company has obtained demand finance loan for the expansion of Hosiery Division – V, disbursed

on March 05, 2020. Repayment of loan is to be made in quarterly installments in 10 years including 02 years

grace period and is secured against Exclusive charge of Rs. 4,000 million (2019: Nil) over land, building and

plant & machinery of Hosiery Division – V of the Company. This exclusive charge is same on both LTFF and

term finance loan facilities from NBP as mentioned in note 26.6 above. Markup is charged at the rate of 06

months KIBOR plus 0.25 % per annum (2019: Nil).

2020 2019

(Rupees ‘000) (Rupees ‘000)

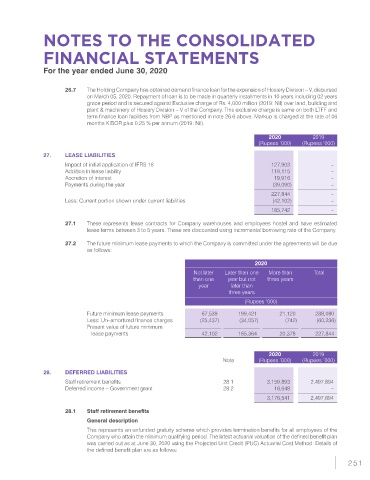

27. LEASE LIABILITIES

Impact of initial application of IFRS 16 127,903 –

Addition in lease liability 119,115 –

Accretion of interest 19,916 –

Payments during the year (39,090) –

227,844 –

Less: Current portion shown under current liabilities (42,102) –

185,742 –

27.1 These represents lease contracts for Company warehouses and employees hostel and have estimated

lease terms between 3 to 5 years. These are discounted using incremental borrowing rate of the Company.

27.2 The future minimum lease payments to which the Company is committed under the agreements will be due

as follows:

2020

Not later Later than one More than Total

than one year but not three years

year later than

three years

(Rupees ‘000)

Future minimum lease payments 67,539 199,421 21,120 288,080

Less: Un–amortized finance charges (25,437) (34,057) (742) (60,236)

Present value of future minimum

lease payments 42,102 165,364 20,378 227,844

2020 2019

Note (Rupees ‘000) (Rupees ‘000)

28. DEFERRED LIABILITIES

Staff retirement benefits 28.1 3,159,893 2,497,894

Deferred income – Government grant 28.2 16,648 –

3,176,541 2,497,894

28.1 Staff retirement benefits

General description

This represents an unfunded gratuity scheme which provides termination benefits for all employees of the

Company who attain the minimum qualifying period. The latest actuarial valuation of the defined benefit plan

was carried out as at June 30, 2020 using the Projected Unit Credit (PUC) Actuarial Cost Method. Details of

the defined benefit plan are as follows:

251