Page 158 - Interloop Annual Report 2018-2019

P. 158

NOTES TO THE UNCONSOLIDATED NOTES TO THE UNCONSOLIDATED

FINANCIAL STATEMENTS FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2019 FOR THE YEAR ENDED JUNE 30, 2019

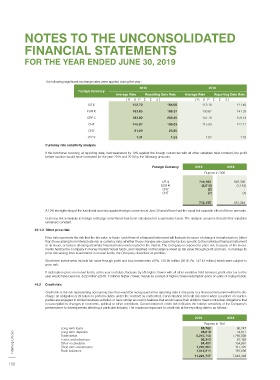

The following significant exchange rates were applied during the year : Loans and advances consist of loans to employees & director and Metis International (Pvt) Ltd. Loans to employees and director are secured against

their retirement benefits and loan to Metis International is also secured through an irrevocable lien/charge on total assets of the Metis International

2019 2018 (Pvt) Limited. Therefore, Company is not exposed to any significant credit risk on these loans.

Foreign Currency

Average Rate Reporting Date Rate Average Rate Reporting Date Rate

Long term deposits have been mainly placed with suppliers of electricity, gas and telecommunication services. Considering the financial position

[ R U P E E S ] [ R U P E E S ] and credit quality of the institutions, Company’s exposure to credit risk is not significant.

US $ 142.70 164.00 113.10 121.40

Trade debts amounting to Rs. 4,251 million out of total debts are secured against letters of credit and insured contract. Furthermore, credit quality

EUR 163.85 186.37 130.62 141.33 of customers is assessed taking into consideration their financial position and previous dealings and on that basis, individual credit limits are set.

GBP £ 183.80 208.45 147.78 159.14 Moreover, the management regularly monitors and reviews customers’ credit exposure. Accordingly, the company is not exposed to any significant

credit risk.

CHF 145.07 168.03 115.83 122.11

Other receivables constitute mainly receivables from the related parties and mark up subsidy from banks. Considering the financial position of

CNY 21.29 23.85 - - related parties and credit quality of banks and insurance company exposure to credit risk is not significant.

JPY ¥ 1.31 1.53 1.02 1.10

Short term investments are investments in mutual funds, TDRs and sales tax refund bonds. The credit risk on these investments is limited because

counter parties are fund management Companies, banks and Government with reasonably high credit ratings. The credit quality of mutual funds

Currency rate sensitivity analysis

can be assessed by reference to external credit ratings or to historical information about counter party default rate.

If the functional currency, at reporting date, had weakened by 10% against the foreign currencies with all other variables held constant, the profit

before taxation would have increased for the year 2019 and 2018 by the following amounts: 2019 2018

[ Credit Ratings ]

Foreign Currency 2019 2018

Rupees in ‘000 Al Meezan Investment Management Limited AM1 AM1

NBP Fund Management Limited AM1 AM1

Alfalah GHP Investment Management Limited AM2+ AM2+

US $ 744,183 662,390 UBL Fund Managers Limited AM1 AM1

EUR (2,019) (1,142)

CNY (2) - The credit quality of Company’s bank balances can be assessed by reference to external credit ratings or to historical information about counterparty

CHF (7) (4) default rate:

742,155 661,244 Name of Bank Date Long term Short term Outlook Agency

A 10% strengthening of the functional currency against foreign currencies at June 30 would have had the equal but opposite effect of these amounts. Allied Bank Limited 27-Jun-19 AAA A1+ Stable PACRA

Askari Bank Limited 28-Jun-19 AA+ A1+ Stable PACRA

Currency risk sensitivity to foreign exchange movements has been calculated on a symmetric basis. The analysis assumes that all other variables Bank Alfalah Limited 28-Jun-19 AA+ A1+ Stable PACRA

remained constant. Burj Bank Limited 28-Jun-19 A A1 Stable PACRA

Dubai Islamic Bank Pakistan Limited 28-Jun-19 AA A-1+ Stable JCR-VIS

49.1.3 Other price risk: Faysal Bank Limited 27-Jun-19 AA A1+ Stable PACRA

Habib Bank Limited 28-Jun-19 AAA A-1+ Stable JCR-VIS

Price risk represents the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices (other Habib Metropolitan Bank Limited 27-Jun-19 AA+ A1+ Stable PACRA

than those arising from interest rate risk or currency risk), whether those changes are caused by factors specific to the individual financial instrument MCB Bank Limited 27-Jun-19 AAA A1+ Stable PACRA

or its issuer, or factors affecting all similar financial instruments traded in the market. The Company is exposed to price risk, because of the invest- MCB Islamic Bank Limited 27-Jun-19 A A1 Stable PACRA

ments held by the Company in money market mutual funds, and classified on the balance sheet as fair value through profit and loss. To manage its Meezan Bank Limited 28-Jun-19 AA+ A-1+ Stable JCR-VIS

price risk arising from investments in mutual funds, the Company diversifies its portfolio. National Bank of Pakistan 28-Jun-19 AAA A1+ Stable PACRA

Silk Bank Limited 27-Jun-19 A- A-2 Stable JCR-VIS

Short term investments include fair value through profit and loss investments of Rs. 130.90 million (2018: Rs. 147.43 million) which were subject to Standard Chartered Bank Pakistan Limited 25-Jun-19 AAA A1+ Stable PACRA

price risk. The Bank of Punjab 28-Jun-18 AA A1+ Stable PACRA

United Bank Limited 28-Jun-18 AAA A-1+ Stable JCR-VIS

If redemption price on mutual funds, at the year end date, fluctuate by 5% higher / lower with all other variables held constant, profit after tax for the

year would have been Rs. 6.22 million (2018: 7 million) higher / lower, mainly as a result of higher / lower redemption price on units of mutual funds.

Due to Company’s long standing relationships with these counterparties and after giving due consideration to their strong financial standing, man-

agement does not expect non-performance by these counter parties on their obligations to the Company. Accordingly, the risk is minimal.

49.2 Credit risk:

49.3 Liquidity risk

Credit risk is the risk representing accounting loss that would be recognized at the reporting date if one party to a financial instrument will fail to dis-

charge an obligation or its failure to perform duties under the contract as contracted. Concentration of credit risk arises when a number of counter- Liquidity risk is the risk that an entity will encounter difficulty in meeting obligations associated with financial liabilities.

parties are engaged in similar business activities or have similar economic features that would cause their ability to meet contractual obligations that

is susceptible to changes in economic, political or other conditions. Concentration of credit risk indicates the relative sensitivity of the Company’s The company’s approach to manage liquidity risk is to maintain sufficient level of liquidity by holding highly liquid assets and the availability of funding

performance to developments affecting a particular industry. The maximum exposure to credit risk at the reporting date is as follows :

through an adequate amount of committed credit facilities. At June 30, 2019 the Company has Rs. 13,224 million (2018: Rs 4,381.56 million) unuti-

lized borrowing limits available from financial institutions and Rs. 1,538.56 million (2018: Rs. 193.69 million) cash and bank balances. The manage-

2019 2018 ment believes that the company is not exposed to any liquidity risk.

Rupees in ‘000

Long term loans 65,762 60,747 2018 - 19

28,019

24,817

Long term deposits

Interloop Limited Trade debts 8,247,740 7,293,008 Annual Report

Loans and advances

66,343

81,163

154,697

94,421

Other receivables

147,425

Short term investments

1,207,251

Bank balances

1,512,211

181,636

11,221,747 7,943,493

156 157