Page 130 - InterloopAnnualReport2021

P. 130

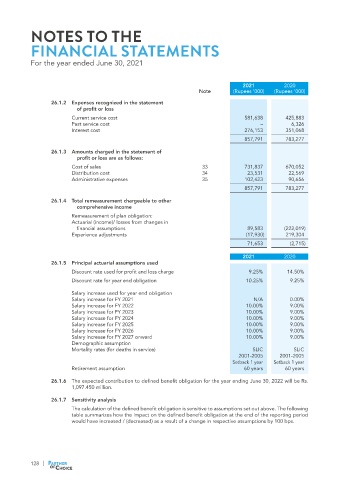

NOTES TO THE

FINANCIAL STATEMENTS

For the year ended June 30, 2021

2021 2020

Note (Rupees ‘000) (Rupees ‘000)

26.1.2 Expenses recognized in the statement

of profit or loss

Current service cost 581,638 425,883

Past service cost – 6,326

Interest cost 276,153 351,068

857,791 783,277

26.1.3 Amounts charged in the statement of

profit or loss are as follows:

Cost of sales 33 731,837 670,052

Distribution cost 34 23,531 22,569

Administrative expenses 35 102,423 90,656

857,791 783,277

26.1.4 Total remeasurement chargeable to other

comprehensive income

Remeasurement of plan obligation:

Actuarial (income)/ losses from changes in

financial assumptions 89,583 (222,019)

Experience adjustments (17,930) 219,304

71,653 (2,715)

2021 2020

26.1.5 Principal actuarial assumptions used

Discount rate used for profit and loss charge 9.25% 14.50%

Discount rate for year end obligation 10.25% 9.25%

Salary increase used for year end obligation

Salary increase for FY 2021 N/A 0.00%

Salary increase for FY 2022 10.00% 9.00%

Salary increase for FY 2023 10.00% 9.00%

Salary increase for FY 2024 10.00% 9.00%

Salary increase for FY 2025 10.00% 9.00%

Salary increase for FY 2026 10.00% 9.00%

Salary increase for FY 2027 onward 10.00% 9.00%

Demographic assumption

Mortality rates (for deaths in service) SLIC SLIC

2001-2005 2001-2005

Setback 1 year Setback 1 year

Retirement assumption 60 years 60 years

26.1.6 The expected contribution to defined benefit obligation for the year ending June 30, 2022 will be Rs.

1,097.450 million.

26.1.7 Sensitivity analysis

The calculation of the defined benefit obligation is sensitive to assumptions set out above. The following

table summarizes how the impact on the defined benefit obligation at the end of the reporting period

would have increased / (decreased) as a result of a change in respective assumptions by 100 bps.

128